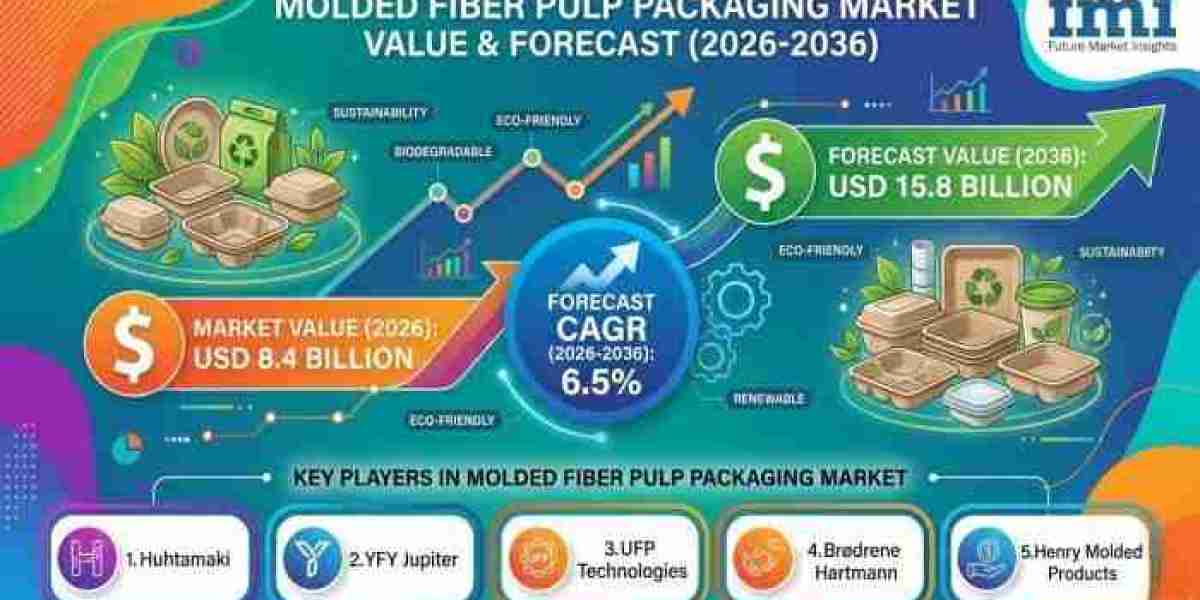

According to the latest market analysis by Future Market Insights, the molded fiber pulp packaging market is rapidly transforming from a secondary packaging alternative into a mainstream solution for protective and food-contact applications. Valued at USD 7.9 billion in 2025 and projected to reach USD 8.4 billion in 2026, the market is expected to expand at a CAGR of 6.5% during the forecast period, ultimately reaching USD 15.8 billion by 2036.

This growth reflects a broader structural shift within the packaging industry, where manufacturers and brands are increasingly transitioning away from plastic-intensive formats toward fiber-based solutions that offer a balance of protection, scalability, and sustainability without requiring major modifications to existing packaging infrastructure.

Get detailed market forecasts, pricing analysis, and competitive benchmarking:

https://www.futuremarketinsights.com/reports/sample/rep-gb-2900

Quick Market Highlights

- Market Value (2025): USD 7.9 Billion

- Estimated Market Size (2026): USD 8.4 Billion

- Forecast Market Value (2036): USD 15.8 Billion

- CAGR (2026–2036): 6.5%

- Incremental Opportunity: USD 7.4 Billion

- Leading End Use Segment: Electronics Packaging (38% Share)

- Dominant Product Type: Transfer Molded Packaging (46% Share)

Market Evolution and Structural Transformation

The molded fiber pulp packaging market is entering a sustained expansion phase, with market value expected to nearly double over the next decade. However, the industry transformation extends beyond numerical growth.

A major shift is occurring in packaging decision-making processes. Plastic trays and inserts, once considered standard across multiple industries, are increasingly being replaced due to rising sustainability concerns and recyclability requirements. Molded fiber packaging is emerging as a practical substitute by delivering comparable cushioning and protective performance while supporting lower plastic dependency and improved environmental positioning.

Unlike disruptive packaging transitions that demand complete operational overhauls, molded fiber solutions integrate efficiently into existing production and logistics systems, making adoption commercially attractive across foodservice, electronics, retail, and industrial sectors.

Key Growth Drivers

- Rising Plastic Reduction Initiatives: Government regulations, sustainability mandates, and corporate ESG commitments are accelerating the transition toward recyclable and fiber-based packaging materials. Molded fiber packaging is gaining traction as a scalable replacement for plastic in high-volume applications.

- Compatibility with Existing Operations: Fiber trays, end caps, clamshells, and inserts can be incorporated into existing packaging workflows with minimal operational disruption, enabling cost-effective implementation.

- Increasing Demand for Recyclable Packaging: Consumers and businesses are prioritizing packaging formats that are easy to recycle and dispose of, particularly within consumer electronics, foodservice, and e-commerce sectors.

Market Challenges and Operational Constraints

Despite strong momentum, the market continues to face several technical and operational challenges.

Performance limitations—including moisture sensitivity, inconsistent surface finish, and dimensional precision issues—can restrict adoption in premium packaging applications. In addition, manufacturing consistency remains critical. Tooling accuracy, drying efficiency, and nesting precision must meet strict quality standards to ensure large-scale repeatability and cost control.

Emerging Opportunity Areas

Several high-growth opportunities are reshaping the competitive landscape:

- Expansion of molded fiber inserts in consumer electronics packaging

- Increasing adoption in takeaway containers and foodservice trays

- Rising use in recyclable protective transit packaging

- Development of advanced thermoformed and dry-molded fiber technologies with improved structural performance and surface quality

Segment Analysis

- By End Use: Electronics packaging leads the market with a 38% share, driven by growing demand for sustainable protective packaging solutions that reduce visible plastic content while maintaining product safety.

- By Product Type: Transfer molded packaging dominates with a 46% market share due to its cost efficiency and suitability for large-scale production.

- By Material: Recycled paper pulp accounts for approximately 62% of the market, supported by strong raw material availability and cost-effective scalability.

- By Packaging Format: Trays hold a 36% market share because of their versatility across food packaging, electronics, and retail applications.

- By Application: Protective packaging remains the leading application segment with a 40% share, as cushioning and product protection continue to drive adoption.

Regional Market Insights

Regional growth trends vary based on manufacturing strength, packaging infrastructure, and sustainability regulations.

- East Asia leads with a 32% market share, supported by export-oriented manufacturing ecosystems

- India is projected to grow at an 8.4% CAGR due to expanding manufacturing activities and strong conversion potential

- China is expected to register a 7.8% CAGR, driven by large-scale production capacity and established converter networks

- Brazil is witnessing growth through increasing demand from agriculture and food packaging industries

- The United States market is projected to expand steadily at a 5.8% CAGR across electronics and foodservice applications

- Germany and the United Kingdom continue to benefit from regulation-driven sustainability initiatives and packaging compliance standards

Competitive Landscape

The market remains fragmented, with competition centered on operational execution and application-specific capabilities.

Key companies such as Huhtamaki, YFY Jupiter, UFP Technologies, Brødrene Hartmann, Henry Molded Products, EnviroPAK, and Novolex are focusing on:

- Advanced tooling precision and faster development cycles

- Consistent product quality and surface finish

- Efficient drying and manufacturing processes

- Custom molded packaging designs for complex applications

In this market, competitive success increasingly depends on reliability, repeatability, and operational efficiency rather than sustainability positioning alone.

Strategic Implications for Stakeholders

- Manufacturers: Investment in tooling optimization, automation, and process consistency will be critical for scaling production efficiently.

- Brands: Companies can strengthen sustainability positioning while reducing dependency on plastic packaging materials.

- Investors: Growth opportunities are emerging across packaging machinery, specialty fiber materials, and custom packaging solutions.

- Procurement Leaders: Supplier evaluation is increasingly focused on scalability, compliance capabilities, and production reliability.

Future Outlook

Over the next decade, molded fiber pulp packaging is expected to evolve from a selective packaging alternative into a standardized packaging format across multiple industries.

Key trends shaping the future include:

- Expansion of thermoformed and dry-molded fiber technologies

- Improved moisture resistance and premium surface finishes

- Integration with automated packaging systems

- Greater adoption in retail-ready and premium packaging applications

As innovation and process optimization continue to improve product performance, molded fiber packaging is likely to transition from a sustainability-driven substitute into a preferred default packaging material across global packaging ecosystems.

Executive Summary

- Molded fiber pulp packaging is transitioning from niche adoption to mainstream usage

- Market growth is driven by plastic reduction initiatives, recyclability demand, and operational compatibility

- Electronics and protective packaging remain primary demand generators

- Tooling precision and production consistency continue to be key operational challenges

- Future competitive advantage will depend on process efficiency, scalability, and material innovation

The next phase of market expansion will be defined by advanced fiber technologies, manufacturing optimization, and the large-scale commercialization of sustainable packaging solutions worldwide.

About Future Market Insights (FMI)

Future Market Insights, Inc. (FMI) is an ESOMAR-certified, ISO 9001:2015 market research and consulting organization, trusted by Fortune 500 clients and global enterprises. With operations in the U.S., UK, India, and Dubai, FMI provides data-backed insights and strategic intelligence across 30+ industries and 1200 markets worldwide.